posted 3rd April 2026

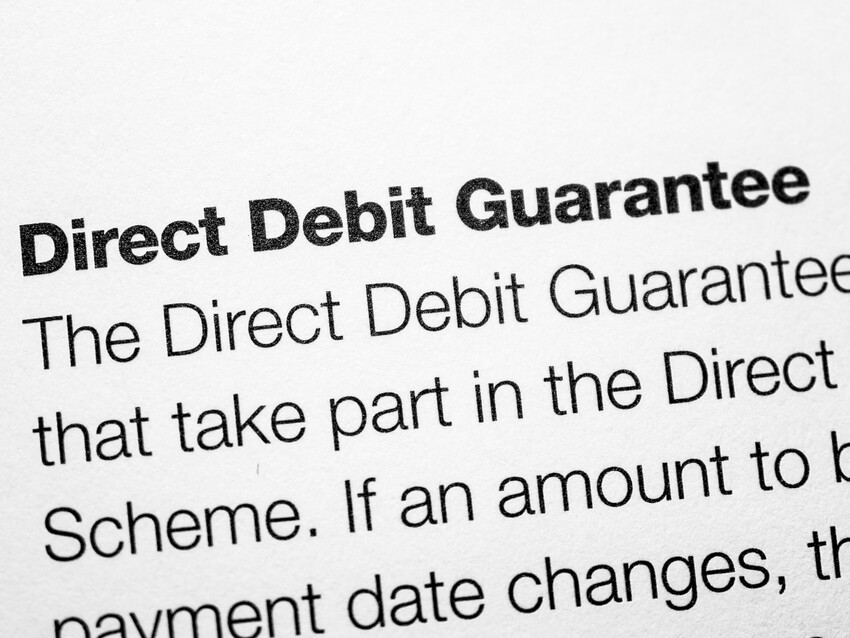

Millions of people in the UK rely on Direct Debit every day, trusting that payments will be taken correctly and that, if something goes wrong, they are protected. At the centre of that trust is the Direct Debit Guarantee, a promise of a “full and immediate refund.”

But what if that promise does not reflect how the system actually works?

Behind the reassurance lies a structure that most consumers never see. The Direct Debit scheme is operated by Bacs Payment Schemes Limited, which is part of Pay.UK. Despite the impression of an independent and protective framework, Bacs is not a regulator, does not investigate fraud, and does not handle consumer complaints.

Instead, it sets the rules for a system heavily shaped by the banking industry itself.

This matters because the same banks that process Direct Debit payments and decide whether consumers receive refunds are also central participants in the scheme’s governance. In effect, the institutions that apply the rules are closely connected to those who shape them. Critics argue that this creates a system that, in practice, marks its own homework.

The Direct Debit Guarantee tells consumers they are protected. It creates the expectation of a simple, automatic safety net. But it does not explain the reality behind that promise.

- It does not say that Bacs will not deal with fraud complaints.

- It does not say that your bank will investigate and may challenge your claim.

- It does not say that refunds can be revisited or reversed.

- It does not say that, if the bank refuses, the consumer may have to escalate the matter to the Financial Ombudsman Service.

In short, it does not explain how the system works when things go wrong.

That gap is not theoretical; it exists in a wider landscape of growing fraud. The Home Office’s Economic Crime Survey 2024 found that 27% of businesses experienced fraud in a single year, with an estimated 6.04 million fraud incidents. Among these was mandate fraud, affecting 7% of businesses , where payment instructions are set up or altered without proper authority. This type of fraud goes directly to the heart of systems like Direct Debit, which rely on pre-authorised mandates rather than real-time verification.

For those dealing with unauthorised payments, the experience can be very different from the simplicity promised. Evidence from consumer helplines and support services suggests a pattern: some refunds are processed quickly, but others are delayed, challenged, or reversed after investigation. Consumers may be passed between banks and companies, sometimes with no clear resolution, particularly where fraudsters are involved.

At that point, the system's structure becomes clear.

- Bacs sets the rules but does not intervene.

- Banks apply and interpret those rules.

- Disputes are pushed outside the system to the Ombudsman.

There is no single body responsible for handling fraud cases from start to finish.

This creates what critics describe as an accountability gap. A system that appears unified to consumers is, in reality, fragmented and in part self-regulated.

The guarantee offers certainty, but the process that delivers it is conditional, variable, and dependent on institutions that are not independent of the system itself.

The issue is not simply whether the Direct Debit Guarantee exists. It is whether it tells consumers enough. The wording is reassuring, but it is not transparent. It gives confidence, but not clarity. It does not reflect who makes decisions, who can refuse a claim, or what a consumer must do if the guarantee is challenged.

Defenders of the system argue that it works in the majority of cases and provides strong protection. But that defence avoids a more fundamental question: who is ultimately accountable when it does not work?

In a system where fraud is widespread, where mandate abuse affects millions of cases, and where responsibility is divided across multiple organisations, trust cannot rely on reassurance alone.

Consumers are entitled not just to protection, but to transparency about how that protection is delivered.

- If Bacs does not deal with fraud complaints, that should be clear.

- If banks both shape and apply the rules, that should be clear.

- If the real route for unresolved disputes is the Ombudsman, that should be clear.

Until that happens, the criticism will remain difficult to ignore. The Direct Debit system appears simple and secure. But when fraud occurs, the reality is more complex, and for some, it raises a fundamental concern: that a system built on trust is not matched by a system built on clear accountability.

Victim of Direct Debit Fraud? Let us know.