posted 17th December 2025

Online shopping is now embedded in everyday life. Consumers expect that when they make a digital purchase, the transaction is transparent, fair and limited to what is presented on screen at the time of payment. Increasingly, that expectation is being undermined by hidden subscription charges online, where consumers unknowingly sign up to recurring payments that only come to light when they appear on a bank statement weeks or months later. This practice is not rare. It is becoming systemic.

Across the UK, consumers are discovering unexpected monthly charges on their bank statements linked to purchases they believed were one-off transactions. While businesses often argue that the subscription was disclosed in their terms and conditions, the reality is that these ongoing payment obligations are frequently hidden in small print, buried within lengthy documents that most consumers never reasonably read during checkout. This is not informed consent. It is consent manufactured through obscurity.

The scale of the issue is significant. Consumer organisations estimate that millions of UK consumers have unknowingly signed up to a subscription after making an online purchase. The combined financial impact of these recurring payments, hidden in the terms and conditions, is measured in billions of pounds each year.These are not deliberately chosen premium memberships. They are subscriptions attached to everyday products, digital downloads, supplements, trial offers and lifestyle goods, all presented in a way that strongly implies a single purchase.

Meridian Legal increasingly sees consumers seeking guidance on how they became locked into an online subscription trap. While the specific facts differ, the scenarios follow a consistent pattern. A consumer completes an online checkout believing they are paying once. There is no explicit warning that the purchase includes an ongoing monthly subscription. No pop-up notice. No mandatory acknowledgement. No interruption to the payment flow. Weeks later, a recurring payment appears on the bank statement.

In one illustrative scenario, a consumer only notices the charge after reviewing several months of statements. The amount is small enough to go unnoticed. By the time it is queried, multiple payments have already been taken. When the consumer contacts the merchant, they are told the subscription was disclosed in the terms and conditions. When they contact their bank, they are advised that the payment has been authorised and must be cancelled directly with the seller. What began as a minor online purchase escalates into a prolonged dispute involving stress, time and financial loss.

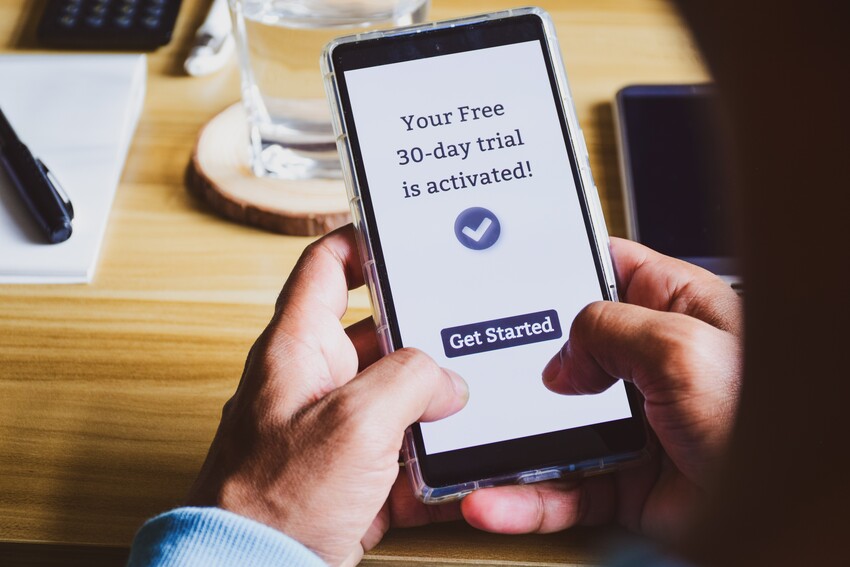

Another commonly reported situation involves so-called free trials. Consumers believe they are paying a nominal amount for postage or access to an introductory offer. What is not made clear at the point of purchase is that failure to cancel will result in ongoing monthly charges. The subscription is technically disclosed, but only within dense legal text that requires deliberate searching. Many consumers do not discover the obligation until the trial has expired and payments have already been taken.

The issue here is not consumer carelessness. It is designed. Subscription consent is engineered to be passive. Recurring payment obligations are concealed within terms and conditions rather than presented clearly at the point of purchase. The checkout journey itself reinforces the impression of a one-time transaction. This is precisely why consumers later say they were unaware they had agreed to a subscription.

From a consumer rights perspective in the UK, this approach is increasingly difficult to defend. The legal argument that information existed somewhere on the website does not align with how real people interact with online platforms. Most consumers do not read full terms and conditions before buying everyday items. Businesses understand this. Regulators understand this. The model depends on it.

Complaint data support this position. Banks continue to receive high volumes of disputes over recurring payments that consumers say they did not knowingly authorise. Trading Standards offices are recording ongoing complaints about subscription charges hidden in the small print. Consumer advocacy groups consistently report that subscription-related disputes are among the most persistent and emotionally charged, particularly when cancellation processes are unclear or obstructive.

In many cases, consumers only become aware of the problem when reviewing a bank statement closely or when a bank fraud monitoring system flags unusual activity. By then, the financial harm has already occurred. Attempts to cancel often involve navigating hidden account areas, delayed responses or conditional refunds that leave consumers feeling trapped.

The regulatory gap is now clear. Existing consumer protection law focuses on whether information is provided, not whether it is presented in a way that enables genuine understanding. In a digital marketplace shaped by behavioural design, that distinction is critical. Transparency in theory does not equal transparency in practice.

There is a practical and proportionate solution.

If an online purchase includes an ongoing subscription, that fact should be made explicitly clear at the point of sale. A prominent on-screen notice should appear before payment is taken. Plain language should be used. For example, this purchase includes an ongoing monthly subscription. You should include a direct hyperlink to the relevant terms and conditions within that notice. Crucially, the consumer should be required to actively acknowledge this before proceeding.

This approach reflects how consumers actually behave online. It does not prevent subscriptions. It simply ensures that consent is real.

Other sectors already operate under stricter disclosure requirements where ongoing financial commitments are involved. Financial services, insurance and credit agreements require layered warnings and active confirmations because the risk of consumer harm is recognised. Online subscription models that rely on recurring payments should be subject to the same standard.

The current reliance on small print places all risk on the consumer. It rewards businesses that design checkout processes to minimise attention on recurring costs. It penalises consumers acting reasonably and in good faith. Regulatory reform must therefore focus on visibility, not just the availability of information. Consent must be active.

Silence, assumption or oversight should no longer be treated as agreement.

Until this changes, complaints about hidden subscription charges online will continue to rise. Banks will remain caught between merchants and customers.

Regulators will continue to intervene after harm has occurred rather than preventing it. Most importantly, consumer trust in online commerce will continue to erode.

Transparency at the point of purchase is not radical. It is basic consumer protection. Say when a subscription applies. Say it clearly. Say it before the money leaves the account.

Anything less belongs in Shark Alley.